Retirement Savings by Age: Are you on track?

If you’ve ever wondered “Am I saving enough for retirement?,” you’re not alone.

It’s one of the most common questions people ask. And unfortunately, the answers you find online are often confusing. Some articles say you need $2 million. Others say $5 million. Some tell you to multiply your income by 10. Others say 25.

It’s enough to make anyone want to close the laptop and take a nap.

The good news is that retirement planning doesn’t have to be complicated. While everyone’s situation is different, there are some general benchmarks that can help you see if you’re on track.

Think of these numbers as guideposts, not strict rules.

Why “Retirement by Age” Benchmarks Exist

Saving for retirement is a long journey. It’s hard to know if you're doing well when the finish line may be 20 or 30 years away.

That’s why planners often look at milestones by age. These benchmarks help answer questions like:

Am I saving fast enough?

Should I increase my savings?

Am I ahead or behind?

Again, these aren’t perfect rules. Life rarely follows a spreadsheet. But they can help you spot problems early while there’s still plenty of time to adjust.

A Simple Retirement Savings Rule of Thumb

If you have a rough idea of your retirement goal, you can break that number into milestones along the way (not sure what your retirement nest egg needs to hit? Check out THIS POST to figure it out!).

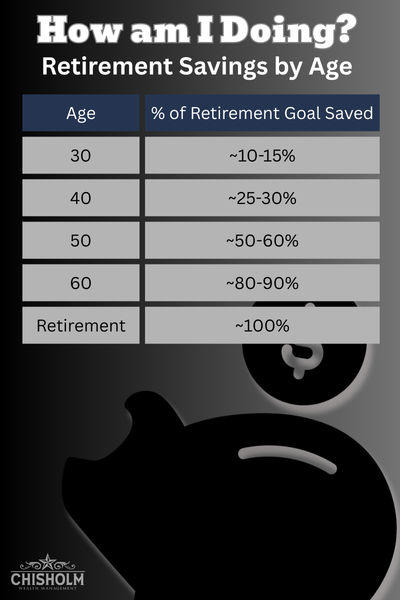

A simple rule of thumb is to think in terms of percentage of your goal saved.

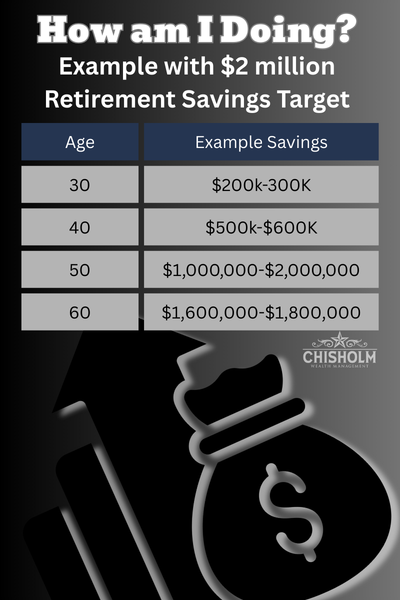

For example, if your retirement target is $2 million, your progress might look something like this:

These numbers aren’t strict rules. Some people start saving later and catch up. Others start earlier and get ahead.

The key point is that progress matters more than perfection.

What Really Matters More Than the Benchmarks

While the age milestones are helpful, they don’t tell the whole story. There are three big factors that matter even more.

1. Your Spending in Retirement

Retirement planning isn’t really about how much money you have.

It’s about how much money you need to spend each year.

For example:

Someone who spends $60,000 per year in retirement will need far less savings than someone spending $120,000 per year. Your retirement lifestyle drives the math.

Some people travel the world. Others are happy with gardening, grandkids, and the occasional trip to Costco. Both can work.

2. How Long You’ll Work

Retiring at 55 requires much more savings than retiring at 67.

Why?

Because you need your money to last longer. Working even a few extra years can dramatically improve your financial picture because it allows you to:

Save more

Delay withdrawals

Possibly increase Social Security benefits

Sometimes the most powerful retirement strategy is simply working a little longer than planned.

3. Investment Growth

Your savings alone rarely funds your retirement. Your investments also do a lot of heavy lifting.

Over time, growth can become the biggest contributor to your retirement account.

For example, someone who consistently saves and invests through their career may find that investment growth eventually contributes more than their actual deposits. This is why starting early is so powerful.

What If You’re Behind?

This is where many people start to panic. They look at a chart like the one above and realize they’re not quite where they hoped to be.

First, take a breath. Retirement planning is not a pass-fail exam.

There are several ways to improve your situation if you’re behind.

Increase Your Savings Rate

Saving a little more each year can make a meaningful difference over time.

For example, increasing your savings from 10% of income to 15% can significantly change your long-term results. Even small increases can help. If you’re old enough, you can also use catch-up contributions to accelerate your retirement savings.

Reduce Future Spending Needs

Sometimes the easiest way to improve your retirement outlook is not saving more.

It’s needing less. This might include:

paying off your mortgage before retirement

reducing unnecessary expenses

downsizing your home later in life

Lower spending means your savings don’t have to work as hard.

Adjust Your Timeline

If retirement at 60 looks difficult, retiring at 65 or 67 may change the picture dramatically.

A few extra working years can mean:

more savings

fewer years withdrawing money

larger Social Security benefits

Sometimes small adjustments create big improvements.

What If You’re Ahead?

First of all - congrats! You’re probably doing something right. But being ahead doesn’t mean you can stop paying attention.

It may allow you to consider options like:

retiring earlier

spending more in retirement

helping family members

charitable giving

The key is making sure your savings are aligned with your long-term goals.

The Problem With Comparing Yourself to Others

One of the biggest mistakes people make is comparing their retirement savings to friends, coworkers, or online statistics. That comparison usually doesn’t help much.

Everyone’s financial life is different.

Different:

income levels

career paths

family situations

spending habits

retirement goals

A better question than “Am I ahead of everyone else?” is: “Am I on track for the life I want?”

Retirement Planning Is About Direction

If there’s one thing to remember, it’s this:

Retirement success rarely comes from one perfect decision.

It usually comes from many small, consistent decisions made over time. Saving regularly, Investing thoughtfully, and making adjustments along the way - That’s what tends to produce good outcomes.

The retirement savings benchmarks we discussed can be helpful reference points. But they are not the full story.

Your ideal retirement plan depends on:

your goals

your spending needs

your timeline

your investment strategy

If you’re unsure whether your current plan supports the future you want, it can be helpful to step back and evaluate the bigger picture.

Sometimes a few thoughtful adjustments today can make a significant difference decades down the road.

Want to make sure you’re on track? Contact us for help.